Luis Felipe de Souza Rodrigues

It’s a highly flexible estimation technique that can be applied in a variety of situations

Hansen (1982) pioneered the introduction of the generalized method of moments (GMM), making notable contributions to empirical research in finance, particularly in asset pricing. The creation of the model was motivated by the need to estimate parameters in economic models while adhering to the theoretical constraints implicit in the model. For example, if the economic model states that two things should be independent, the GMM will try to find a solution in which the average of their product is zero. Therefore, understanding GMM can be a powerful alternative for those who need a model in which theoretical conditions are extremely important, but which conventional models cannot satisfy due to the nature of the data.

Concepts

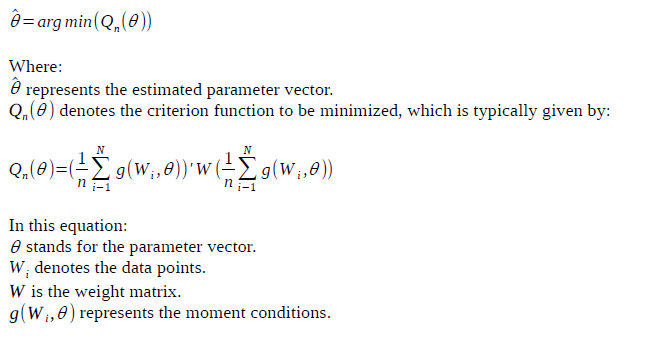

This estimation technique is widely used in econometrics and statistics to address endogeneity and other issues in regression analysis. The basic concept of the GMM estimator involves minimizing a criterion function by choosing parameters that make the sample moments of the data as close as possible to the population moments. The equation for the Basic GMM Estimator can be expressed as follows:

The GMM estimator aims to find the parameter vector θ that minimizes this criterion function, thereby ensuring that the sample moments of the data align as closely as possible with the population moments. By optimizing this criterion function, the GMM estimator provides consistent estimates of the parameters in econometric models.

Being consistent means that as the sample size approaches infinity, the estimator converges in probability to the true parameter value (asymptotically normal). This property is crucial for ensuring that the estimator provides reliable estimates as the amount of data increases. Even in the presence of omitted variables, as long as the moment conditions are valid and instruments are correctly specified, GMM can provide consistent estimators. However, the omission of relevant variables can impact the efficiency and interpretation of the estimated parameters.

To be efficient, GMM utilizes Generalized Least Squares (GLS) on Z-moments to improve the precision and efficiency of parameter estimates in econometric models. GLS addresses heteroscedasticity and autocorrelation by weighting observations based on their variance. In GMM, Z-moments are projected into the column space of instrumental variables, similar to a GLS approach. This minimizes variance and enhances parameter estimate precision by focusing on Z-moments and applying GLS techniques.

Assumptions

However, it is important to recognize that the GMM estimator is subject to a series of assumptions that must be considered during its application, which have been listed:

- Existence of Moments: Up to a certain order is necessary and requires finite tails in the distribution of the data.

- Correct Model Specification: The underlying model must be correctly specified, including the functional relationship and the distribution of error terms.

- Identifiability: There must be a unique solution for the parameters to be estimated.

- Moment Conditions: It is necessary to specify the moment conditions correctly, which must have zero mean under the model assumptions.

- Valid Instruments: If applicable, instruments must be relevant and valid.

- Independence and Homoscedasticity (conditional): Ideally, errors should be independent and homoscedastic under the moment conditions.

- Robustness to Heteroscedasticity: GMM is robust to heteroscedasticity if the weighting matrix is consistently estimated.

- Multicollinearity: GMM can handle multicollinearity, but it can affect the efficiency of the estimators.

- Outliers: GMM is sensitive to outliers unless they are properly addressed in the modeling process.

- Large Samples: GMM is more efficient in large samples.

- Asymptotic Theory: Properties such as consistency and efficiency are asymptotic.

When to use

Therefore, GMM is a highly flexible estimation technique and can be applied in a variety of situations, being widely used as a parameter estimation technique in econometrics and statistics. It allows for efficient estimation of parameters under different model specifications and data structures. Its main uses are:

- Models with Instrumental Variables: used when there are endogenous variables in a model. It provides a way to correct bias in parameter estimation when explanatory variables are correlated with the error.

- Models with Measurement Errors: GMM can be used to correct bias introduced by measurement errors in variables.

- Models with Moment Restrictions: In some situations, there are multiple moment conditions that a model must satisfy. GMM allows you to use all this information simultaneously for more efficient estimation.

- Time Series Models: GMM is often applied in ARMA (AutoRegressive Moving Average) models and other time series models.

- Panel Data Models: It can be used in panel data models to handle issues like heteroscedasticity and autocorrelation within cross-sectional units.

- Nonlinear Models: GMM is also extendable to nonlinear models, providing a robust estimation technique when classical methods like Maximum Likelihood may be infeasible.

Comparing to OLS

The contrast between the Ordinary Least Squares (OLS) method and the Generalized Method of Moments (GMM) points out different advantages. OLS proves itself efficient under the classical assumptions of linearity, serving as an unbiased linear estimator of minimum variance (BLUE). The fundamental assumptions of a linear regression model include: linearity in the relationship between variables, absence of perfect multicollinearity, zero mean error, homoscedasticity (constant variance of errors), non-autocorrelation of errors and normality of errors. Therefore, OLS is an unbiased, consistent and efficient estimator. Furthermore, it have relatively lower computational complexity.

However, GMM provides more flexibility, which is applicable to a wide range of contexts such as models with measurement errors, endogenous variables, heteroscedasticity, and autocorrelation. It makes no assumptions about the distribution of errors and is applicable to nonlinear models. GMM stands out in cases where we have omitted important variables, multiple moment conditions, nonlinear models, and datasets with heteroscedasticity and autocorrelation.

Comparing to MLE

Conversely, when comparing GMM and Maximum Likelihood Estimation (MLE), it highlights their approaches to handling data assumptions. GMM constructs estimators using data and population moment conditions, providing flexibility and adaptability to models with fewer assumptions, particularly advantageous when strong assumptions about data distribution may not hold.

MLE estimates parameters by maximizing the likelihood of the given data, depending on specific assumptions about data distribution. While MLE performs optimally when the assumed distribution closely aligns with the true data-generating process, GMM accommodates various distributions, proving valuable in scenarios where data may not conform to a single specific distribution.

Estimation in Python

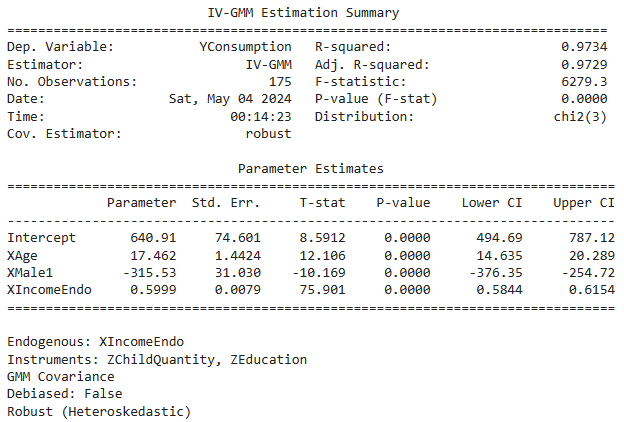

In the hypothetical example demonstrated in Python, we utilize the linearmodels.iv library to estimate a GMM model with the IVGMM function. In this model, consumption serves as the dependent variable, while age and gender (represented as a dummy variable for male) are considered exogenous variables. Additionally, we assume that income is an endogenous variable, while the number of children and education level are instrumental variables.

import pandas as pd

from linearmodels.iv import IVGMM

# Read the Excel file

df = pd.read_excel('example.xlsx')

# Dependent variable

dependent = 'YConsumption'

# Exogenous variables

exog_vars = ['XAge', 'XMale1']

# Endogenous variable

endog_vars = ['XIncomeEndo']

# Instrumental variables

instruments = ['ZChildQuantity6', 'ZEducation']

# Construct the formula for GMM

formula = "{dep} ~ 1 + {exog} + [{endog} ~ {instr}]".format(

dep=dependent,

exog='+'.join(exog_vars),

endog=endog_vars[0],

instr='+'.join(instruments)

)

# Estimate the GMM model

model = IVGMM.from_formula(formula, df)

result = model.fit(cov_type='robust')

# Displaying GMM results

print(result)

Instrumental variables in GMM models are used to address endogeneity issues by providing a source of exogenous variation that is correlated with the endogenous regressors but uncorrelated with the error term. The IVGMM function is specifically designed for estimating models in which instrumental variables are used within the framework of GMM.

Therefore, by specifying Consumption as the dependent variable and employing exogenous variables (age and gender) along with instrumental variables (number of children and education) to address endogeneity, this example fits within the GMM context.

In conclusion, the Generalized Method of Moments (GMM) is seen as a powerful and versatile technique in both econometric and statistical applications, giving it a certain advantage over other methods in some cases. In contrast to the traditional OLS and MLE methods, this method allows for a wider range of model specifications and data structures, as it is less restricted in the assumptions that are required to be satisfied.

In cases of endogeneity, measurement errors, momentum constraints, GMM is especially advantageous. Furthermore, the model performs better in the presence of non-linearities and issues of heteroscedasticity and autocorrelation in the data. GMM utilizes moment conditions and instrumental variables that provide consistent and efficient parameter estimates and is therefore a great alternative of choice for empirical researchers where theoretical conditions are critically important and common methods are not applicable due to violated assumptions or complex data structures.

Therefore, GMM becomes a versatile measurement tool that is suitable for a wide range of empirical settings, allowing researchers to adequately handle complex modeling tasks and provide correct estimates of model parameters.

References

Hansen, L. P. (1982). Large Sample Properties of Generalized Method of Moments Estimators. Econometrica, 50(4), 1029–1054. https://doi.org/10.2307/1912775

Why and When to Use the Generalized Method of Moments was originally published in Towards Data Science on Medium, where people are continuing the conversation by highlighting and responding to this story.

Originally appeared here:

Why and When to Use the Generalized Method of Moments

Go Here to Read this Fast! Why and When to Use the Generalized Method of Moments